Disruption is coming and it’s no joke.

Since the publication of my White Paper, What Next For Financial Planning In The UK? I’ve had numerous in-depth conversations with owner-advisers about the opportunities and threats independently-owned businesses might face from disruptors.

The vast majority of financial planners keep telling me that things are great, and although they claim to understand where I’m coming from, they’re not ready or willing to make changes in response to future threats. Business as usual looks too good.

This is exactly the problem I was trying to highlight in my White Paper. Disruption can look more like a joke than a threat for a long, long time. But then…

It’s due to the exponential nature of disruption.

Watch this short video as I explain it in less than 3 minutes:

Rob Kingsbury, who helped me edit the White Paper, collated some significant market movements throughout 2021 that show the direction of travel for our competitors:

March: Royal London acquires Wealth Wizards

March: Hub Financial Solutions (JUST Group) launches Destination Retirement

April: Octopus acquires financial coaching business Hatch

April: Vanguard launches into UK digital-advice market

May: Ignition enters market

June: JP Morgan buys Nutmeg

August: abrdn buys Exo Investing

December: abrdn acquires interactive investor

M&G are launching a hybrid advice service that was expected in Q4 2021.

Quilter are launching a hybrid advice service in 2022.

There would appear to be a clear market direction here. Big companies with deep pockets are looking to sweep up the wealth-accumulating mass affluent and High Net Worth (HNW) clients of the future, at an early stage in their wealth journey – and before they appear on financial planners’ radars.

Here’s The Challenge For Advisers

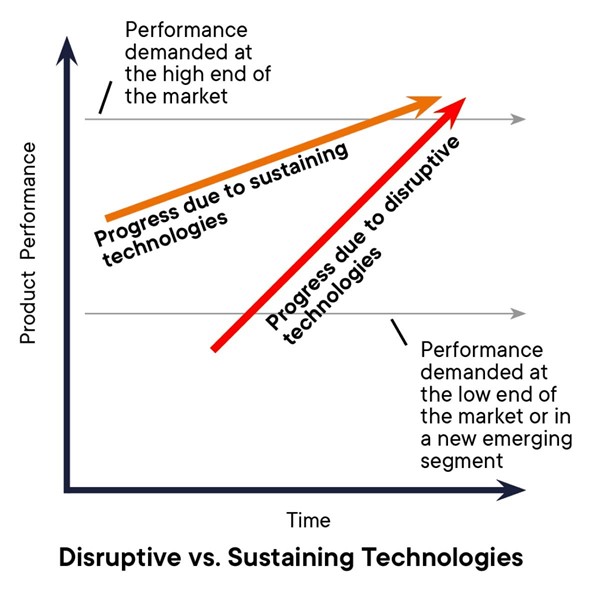

The following chart from Clayton Christensen’s book, The Innovator’s Dilemma, captures the challenges that incumbents face. And let me use financial planning as the example here just to make it relatable.

The top horizontal line in the chart shows the performance demanded by clients at the high end of the market.

The orange upward tilting line that starts below it and eventually crosses it, shows progress due to sustaining technologies. Sustaining technologies advance the current business model’s delivery to existing customers. Basically, they let you do what you currently do, but better.

One might argue that 25 years ago the emerging profession of financial planning was earlier on that darker upward line and below the performance demanded at the high end of the market.

Due to the improvements made to the way financial planners did their job, for example using cashflow forecasting and wrap platforms, and new services that were added to the mix, I believe that the best financial planning firms now meet or exceed the performance demanded from the high-end clients that they serve.

Christensen argues that adding new services above this level will yield no real benefits for the incumbent firms. Clients won’t pay more for things they don’t want or need. So adding to the existing service becomes a drain on profitability.

The lower horizontal line shows the performance demanded at the low end of the market, or in a new emerging segment.

The more vertically angled red line shows progress due to disruptive technologies. Disruptive technologies do something different (often worse) for an unserved or seemingly unprofitable group of customers, often at a poor margin.

As you can see, a new disruptive technology may be below the minimum level of performance demanded by the low end of the market when it first launches.

However, playing in this low oxygen, low profitability space unopposed allows new entrants time to find out where their disruptive approach might resonate best; the fail fast approach, espoused by tech companies.

Once the disruptor does gain a foothold at the bottom end of the market, they can start to move into the next level and over time become genuine competitors for the established players.

If we assume that in today’s world new entrants are digital and have the ability to grow exponentially (if successful) then they can fly below the radar initially, yet become a major threat suddenly as they gain traction.

This is the well-trodden path of disruption.

What To Do?

I outline strategies for different advisory firms in my White Paper (click here to read or listen to it now).

If you’re looking for some new ideas on how you might serve new market segments (like Millennials and Gen Z who are still accumulating wealth) then here are two interesting pieces of tech and a book that might challenge your thinking.

Just to be clear, I haven’t invested in either of these tech pieces and I’m not receiving any other inducements. I just liked them and wanted to share them with you. You’ll need to do your own due diligence and see if they fit your business model.

- Tech: AdviceBridge

AdviceBridge describes itself as a platform that helps advisers automate “the financial planning process” cutting onerous re-keying, admin and time, allowing them to focus on the client relationship instead.

It’s designed to be used as a hybrid advice platform, which mixes human and digital, undertaking many of the monotonous tasks that an administrator, paraplanner and adviser can do.

I’ve seen a demo and it looks super cool. You might want to take a look for yourself and see if it assists you on your innovation journey. You can find out more here.

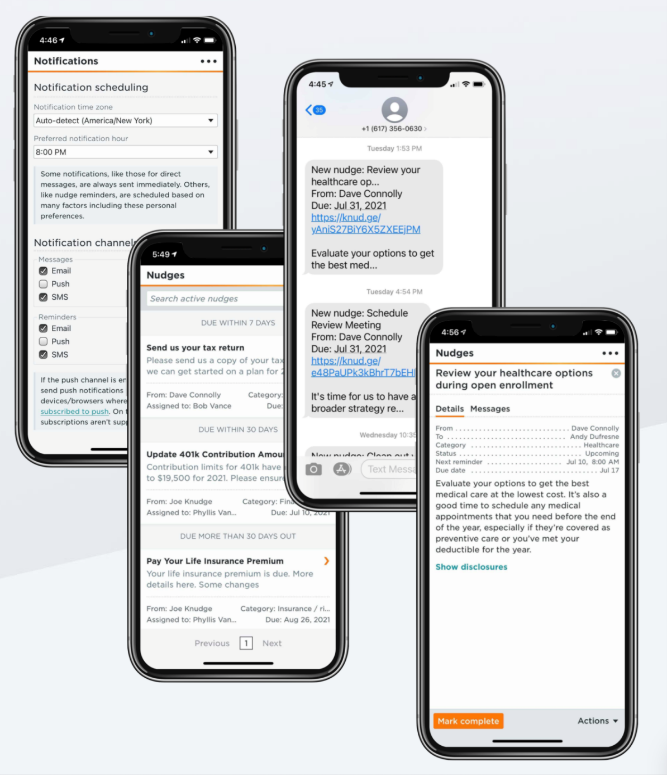

- Tech: Knudge

Knudge assigns action items for your clients, provides a shared to-do-list and sends timely reminders to keep everyone (adviser and client) on the same page. The idea is to dramatically increase follow through of the action items needed to make the financial plan work.

Clients receive reminders via email or text. They can also set their preferences for when and how they’d like to receive reminders and see a shared to-do-list of assigned tasks.

I really loved it as an idea and Dave Connolly who developed it with one of his adviser friends is a super nice guy.

3. Book: A Matter Of Time

Mark Berg and Matthew Jackson have written a fantastic book on why an hourly rate business model makes sense for good quality financial planning businesses.

I have to be honest, I’ve spent 30 years telling myself “I’ll never charge hourly rates”. And then I read this book.

While I haven’t quite drunk enough cool-aid to tell everyone to change to an hourly rate model, the argument here is clearly and powerfully laid out.

Where I think this may have application is for anyone contemplating new business models for new market segments. (That’s my view, not the author’s).

Read it yourself and prepare to be challenged (in a good way). Maybe it will open up some new lines of thinking for you.

Onward

I know there are lots of moves being made in the marketplace right now. If you want to share an idea, a new piece of tech, or debate a point of view, please do reply to this email and let me know your thoughts.

If you’re not already signed up to what Phil Young called “the best free content in the profession” you’re missing out. Get it first by signing up here. (You can leave anytime, although I don’t think you’ll want to)

3 comments to " Disruption Is No Joke "